|

| Image: winteamb |

{kind=link}

In Hong Kong, horse racing is nothing less than an institution. Every year, the Hong Kong Jockey Club conducts over 700 races, bringing in upwards of HKD 100 billion in betting turnovers. This makes the betting market ripe for some economic analysis. In this post, I will be investigating whether the market upholds the conditions for efficiency and rational behaviour. Economics, of course, assumes that human behaviour is consistent and rational. This blog has scrutinised this assumption previously, but this analysis will be done with specific reference to data from horse racing in California and in Hong Kong. The findings that inspired this blog post come from California (refer to "Further reading" below). To determine whether the betting market in Hong Kong displayed similar results, I analysed over 50,000 non-unique horses in more than 4,000 races spanning a six-year period from 2010 to 2015. (A detailed report on that analysis is in progress.)

The betting market is particularly well-suited to an analysis of rationality because each wager has a defined termination point at which its value becomes certain, and bets cannot be traded. It is comparatively difficult to assess rationality in the real estate and financial markets, because the values of those assets are dependent on the present value of future cash flows and the price someone else would be willing to pay. (Refer to The State and the Stock Market for more on "rational bubbles.")

The betting market exhibits qualities very conducive to efficiency: quick, repeated feedback, and a relatively high-stakes environment. Under such conditions, market agents have plentiful opportunities for learning and, given that not insignificant amounts of their own money is on the line, are faced with strong incentives to improve their performance.

It is worth noting that betting on horses, although by no means an exact science, is far removed from playing on the roulette tables. The outcomes of races are not random, and betting pundits abound—one need only refer to the Racing Post published weekly by the South China Morning Post to get a taste of this.

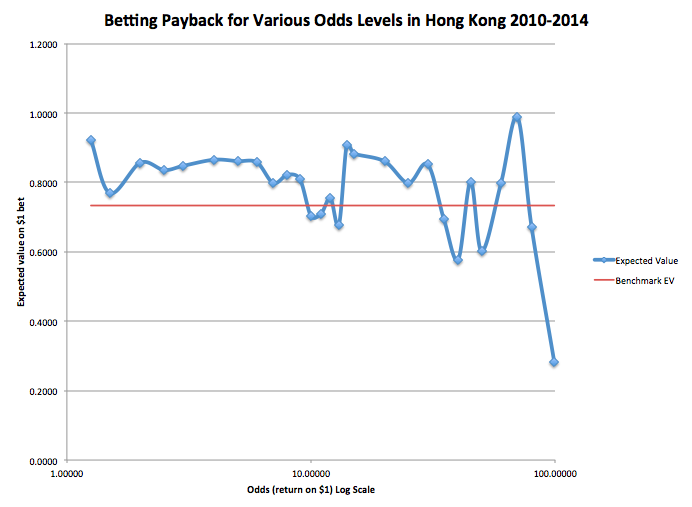

For the market to be considered efficient, all bets must have an expected value of (1-t) times the amount of the bet, where 't' represents the transaction cost involved in the bet. If, for example, the costs attached to a bet equal twenty percent of its value, then in an efficient market bets at all odds levels would return an average of eighty cents to the dollar. If the data show otherwise, then the market is inefficient. Is the pricing of bets consistent with the hypothesis of efficiency?

It turns out that despite a helpful environment, the betting market exhibits significant deviations from efficiency. The most established bias is known as the "favorite-longshot bias," which results in "favourites" winning more often than their odds levels imply, and "long shots" less often. Take two horses, the first with odds of 2 (or 1/1) and the second with odds of 50 (or 49/1). The first would be expected to win one out of every two races in the long run, and the second one out of every fifty. However, the first horse generally ends up winning more than the fifty percent of races expected by the market, and the second horse is victorious less often than the expected two percent.

The excitement of betting on a "long shot"—a horse which the market judges unlikely to win—in the hopes of scoring a large windfall induces many to place their hopes on underdogs (underhorses?). This effect is magnified by what Daniel Kahneman's and Amos Tversky's "prospect theory" has postulated to be a human inability to accurately assess probabilities. Their research suggests that the average gambler is largely unable to differentiate between a 1-in-70 chance and a 1-in-90 chance. The market thus ends up overvaluing long shots, causing them to return less than the benchmark expected value of $(1-t) in the long run.

Favorite-longshot bias was very evident in the analysis of Californian races. In California, the benchmark expected value was 84.67 cents on the dollar, implying transaction costs of 15.33 cents on every dollar bet. As expected, the results do not show a stable expected value across all odds levels. Rather, as the expected returns per dollar bet decrease, the odds lengthen at an ever greater pace. This seems a strong refutation of the idea that the market is efficient.

|

| Figure: Thaler and Ziemba |

The data from Hong Kong, however, do not show nearly as clear a pattern. The expected value for bets was relatively stable for odds levels up to around 70, before spiking sharply and then immediately plunging. Hong Kong's betting market seems to be more sophisticated than California's, with the expected value for most bets clustered around the benchmark value of 73 cents to the dollar. (This value was derived by dividing the total betting payout by the total amount bet, yielding the average expected value of a bet after fees and taxes.) Interestingly, it seems that a large number of knowledgeable bettors are making greater than the expected value of their bets by taking advantage of those betting on horses which win even less than their long odds suggest—the expected value for bets on horses with odds between 80 and 99 is a meagre 28 cents to the dollar. Those who bet on long shots and lose are simply inflating the winning pool for more savvy bettors.

|

| Spreadsheet with data used to create this graph will be made available soon. |

What is the implication of these data for the assumption that economic agents are rational? The data from Hong Kong do not support as strong a conclusion as the data from California. It is very possible that California's betting market is less developed than Hong Kong's. If this assumption holds true, then Hong Kong bettors are wagering in a higher-stakes environment and are on the whole more educated about horse racing. As a result, Hong Kong's betting market displays greater efficiency. This would explain why bets placed with the HKJC yield close to the benchmark expected value at most odds levels.

So, what is the verdict? Are humans rational agents when faced with high stakes and repeated opportunities to learn, as is the case in the betting market? California's data provide evidence that even in such ideal conditions human irrationality prevails, whereas the Hong Kong data display a marked move toward rationality. The proverbial jury is still out.

Further reading:

Anomalies - Parimutuel Betting Markets: Racetracks and Lotteries (Richard Thaler and William T. Ziemba)

nice

ReplyDelete